Join the Crew

Get the best resources for producers delivered to your mailbox

Get the best resources for producers delivered to your mailbox

According to the Economic Policy Institute, an estimated 10-15% of employers misclassify at least one worker as an independent contractor. Whether intentional or not, misclassification is a crime that can result in serious financial penalties and, in some cases, jail time.

Enter: worker classification tests. Implemented by each state, worker classification tests define whether or not your worker is an independent contractor using simple criteria.

In this post, we cover the two major tests used in the United States, along with a list of which state they’re used in.

To determine your worker’s classification, you’ll need to vet the job according to your state’s labor law test.

Once you’ve determined your worker’s status, you’ll have to pay each worker very differently.

Generally, employees have greater labor protections according to the law. Employees are entitled to benefits such as:

Independent contractors, on the other hand, are handed a lump sum for their work, which they report on a 1099. They are not given any benefits, and their employer doesn’t pay any part of their taxes as part of their payroll.

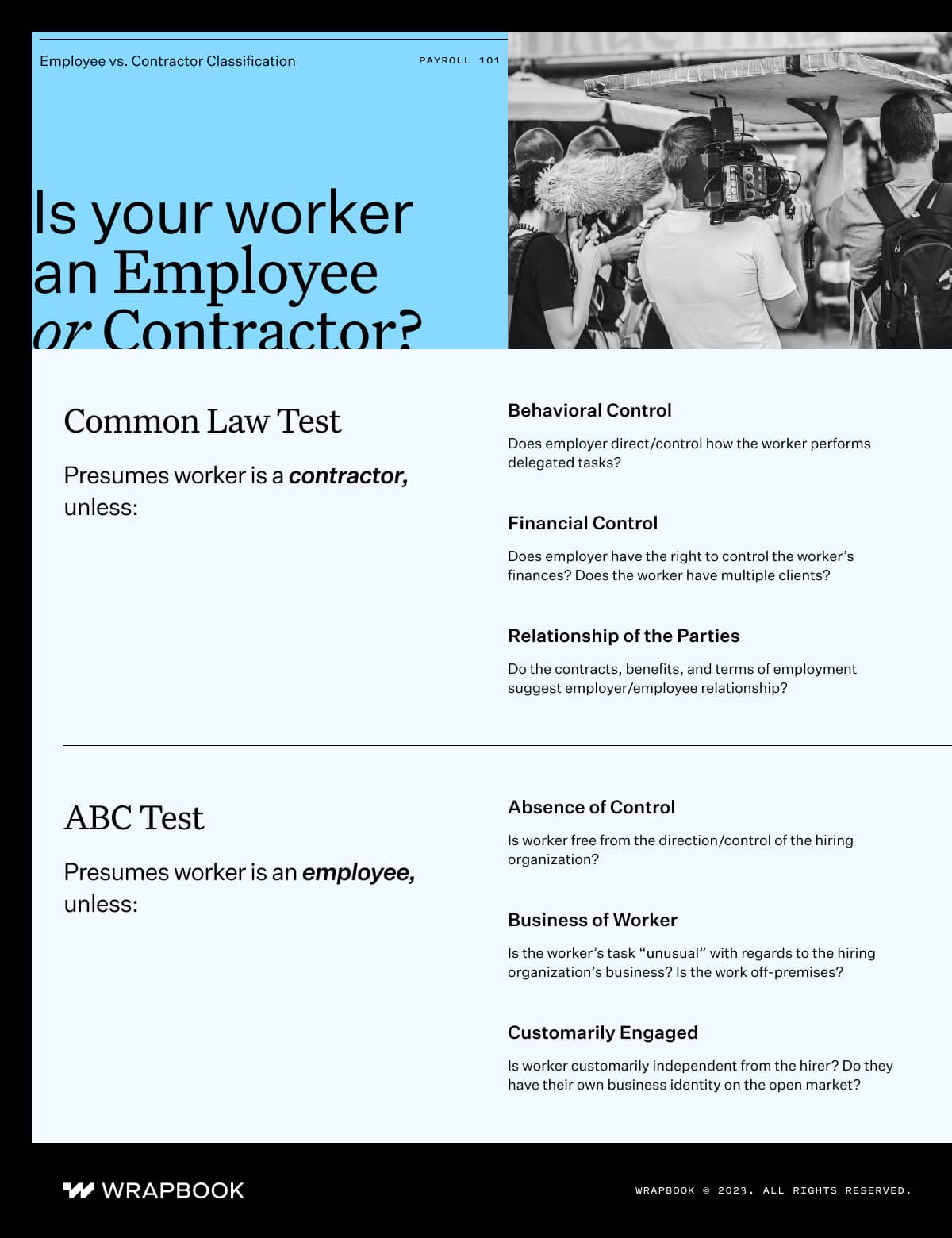

One test some states use to determine worker status is the Common Law Test.

Used by the IRS, New York, the District of Columbia, and 17 other states, the Common Law Test determines worker status by examining behavioral control, financial control, and relationship of the parties for each job.

If an employer wields any of these controls over the worker, then said worker is an employee.

Behavioral control exists when an employer directs and/or controls how his or her workers perform the tasks they’ve been hired to do.

Common examples of behavioral control can include where the work is done, when the work is done, and how the work is done, especially when it comes to a code of conduct.

Even when the employer doesn’t set parameters, behavioral control can still exist. Additionally, just because a worker is highly competent and does not require much supervision or training doesn’t affect the employer’s rights of control.

Financial control exists if employers have a right to control their workers’ finances.

Do you reimburse your worker’s expenses? Do you provide your worker with facilities or equipment? Can your employee experience both profit and loss? The extent of these factors can determine financial control.

Financial control is also determined by if your worker is providing the same services on the open market. In other words, is your employee performing the same functions for multiple clients at once?

Relationship of the parties examines how the worker and employer operate. If your relationship sounds like it's an employee-employer relationship, then your worker is probably an employee.

But how do you prove that? Several ways.

A crucial determinant of party relationship is whether the worker’s business is out of the usual course of the employer’s business.

For example, a painter hired to paint a bank would likely be an independent contractor, as the function of a bank isn’t to paint. However, a painter working for a painting company could be an employee, since painting is a crucial part of a painting company.

Like the Common Law Test, the ABC Test is yet another way states determine your worker’s status as either a contractor or employee.

Currently, the U.S. Department of Labor and 33 states use the ABC Test. Most recently, California changed from Common Law to this test.

The ABC test uses three factors that are in some ways similar to portions of Common Law.

The ABC test presumes a worker is an employee unless the facts and circumstances provide evidence of independent contractor status based on the criteria.

Absence of control exists if the worker is free from the direction or control of the hiring organization both by contract or agreement and in fact.

There are, however, minor exceptions. For example, the hiring organization may set some hours, because of access restrictions. Yet, it still may not direct the worker in how the work is to be performed.

To be classified as an independent contractor, the worker must perform work that is “unusual” in regards to the employing organization’s business and/or off the hiring entity’s premises.

For example, an attorney working for a restaurant as outside counsel would be an independent contractor. The work is unusual compared to the restaurant’s regular business and performed off site at the attorney’s office.

Additionally, painters hired to paint the inside of a bank would still be independent contractors. Even though they are performing their work at the employer’s office, their work is still unusual compared to the bank’s trade.

Various professions and trades are customarily independent contractors available on a per-job basis. They have their own business identity and engage in business for profit on the open market.

The Department of Labor also looks at what they call “economic realities.” The more dependent the worker is on a particular employer for income, the more they lean towards employee status.

By the way regulations are worded, it’s possible for a worker to be an independent contractor under Common Law and an employee under the ABC Test.

For example, an employee can be classified as an independent contractor by the IRS. However, when trying to get covered for unemployment, that same worker could be classified as an employee, because the state (who handles unemployment) uses the ABC Test.

Currently, each state has its own adopted test it uses to determine worker status.

States like California along with the Department of Labor use the ABC Test to determine worker status, while Common Law is the method for both New York and the IRS.

Still, some other states have their own method of determining worker status. In our list of classification tests by state, you’ll notice that some states only abide by specific parts of the ABC test (marked A,B,C). It’s important to pay particular attention to these state regulations.

Whether you end up using the ABC Test or the Common Law Test, knowing your workers’ correct classification is essential to running accurate payroll and shielding yourself from potential lawsuits.

Now that you’ve identified what your employees and contractors ARE, it’s time to pay them. Not sure how to do that? Our practical guide to running film payroll has you covered.

At Wrapbook, we pride ourselves on providing outstanding free resources to producers and their crews, but this post is for informational purposes only as of the date above. The content on our website is not intended to provide and should not be relied on for legal, accounting, or tax advice. You should consult with your own legal, accounting, or tax advisors to determine how this general information may apply to your specific circumstances.

The Wrapbook Team consists of individuals who are thrilled about building modern software tools for creators. We’re a team of compassionate and curious people dedicated to solving complex problems with sophisticated solutions. You can find us across the U.S. and Canada.